Is it possible to pay taxes with a credit card?

You might be curious about whether you can charge your taxes to a credit card. Using a rewards credit card for this could potentially earn you cash back, points, or travel miles.

Your estimated tax payments are usually due on the following schedule:

- From January 1 to March 31: Due by April 15

- From April 1 to May 31: Due by June 15

- From June 1 to August 31: Due by September 15

- From September 1 to December 31: Due by January 15 of the next year

While using a credit card to pay your taxes often incurs service fees and other charges, it might still be beneficial for several reasons.

Subscribe for updates on exclusive offers and discover our editors’ top credit card selections in our daily newsletter.

For example, you may need to meet a minimum spending requirement to qualify for the welcome bonus on a new card or to earn perks like elite-qualifying miles with an airline card or a free night reward with a hotel card.

Alternatively, you might have a card that offers a 0% annual percentage rate on purchases for a limited time, giving you extra time to settle your balance.

There are many reasons you might consider using a credit card to pay your taxes, but there are also important considerations. Here’s what to keep in mind as you weigh your options.

Top credit cards for tax payments

- The Business Platinum Card® from American Express: Ideal for securing a substantial welcome bonus

- The Blue Business® Plus Credit Card from American Express: Top choice for small businesses with no annual fee (refer to rates and fees)

- Chase Freedom Unlimited®: Perfect for those holding an Ultimate Rewards-earning card

- Ink Business Unlimited® Credit Card: Best for enterprises with an Ultimate Rewards-earning card

- Discover it® Miles: Great for cash back during the initial year

The details regarding Discover it Miles and PayPal Cashback Mastercard have been independently gathered by Dinogo. The information on this page has not been validated or endorsed by the card issuer.

A look at the leading credit cards suitable for tax payments

Here, you'll discover the typical earning rates for the top credit cards that allow tax payments, alongside TPG's September valuations of the worth of your accumulated rewards.

Remember that the potential return is also influenced by maximizing earnings as outlined in the "Caveat" section — though it doesn't account for any welcome bonus you may qualify for. We also consider a 1.82% fee for credit card tax payments (further details below).

| Card | Earning Rate | Potential return | Net after 1.82% fee | Caveat |

|---|---|---|---|---|

| The Business Platinum Card from American Express | 1 Membership Reward point per dollar spent. Terms apply | 2% | 0.18% | 50% points bonus on eligible transactions over $5,000 (up to $2 million of these purchases per calendar year, then 1 point per dollar thereafter) |

| The Blue Business Plus Credit Card from American Express | 2 Membership Rewards points per dollar spent (on the first $50,000 in purchases each calendar year; then 1 point per dollar thereafter). Terms apply | 4% | 2.18% | Earning 2 points per dollar is limited to $50,000 in purchases per calendar year, then 1 point per dollar thereafter |

| Chase Freedom Unlimited | 1.5% cash back | 3.08% | 1.26% | Potential value calculated for combining with points from an Ultimate Rewards-earning card |

| Ink Business Unlimited Credit Card | 1.5% cash back | 3.08% | 1.26% | Potential value calculated for combining with points from an Ultimate Rewards-earning card |

| Discover it Miles | 1.5 miles per dollar spent | 3% | 1.18% | Accounting for the first-year cardholder earnings match |

| Chase Sapphire Preferred | 1 Ultimate Rewards point per dollar spent | 2.05% | 0.23% | N/A |

| Capital One Venture Rewards Credit Card | 2 Capital One miles per dollar spent | 3.7% | 1.88% | N/A |

| Capital One Venture X Rewards Credit Card | 2 Capital One miles per dollar spent | 3.7% | 1.88% | N/A |

| Capital One Spark Miles for Business | 2 Capital One miles per dollar spent | 3.7% | 1.88% | N/A |

| PayPal Cashback Mastercard | 3% cash back | 3% | 1.18% | Must pay with this card through PayPal |

If your convenience fees can be deducted as a business expense (consult your tax adviser about this option), your overall benefits could increase significantly.

Various methods to settle your tax obligations

When facing tax payments to the IRS, you have several options available. Most individuals choose from the following methods:

- You can initiate a direct payment from your bank account, and the IRS won’t apply any additional fees for this method

- You can transfer funds from a bank account, though this option often comes with a fee

- You can send a check or money order to the IRS without incurring any fees aside from postage and potentially the cost of the money order (depending on the source)

Should you require additional time to settle your taxes, you can apply for an extension with the IRS or establish an installment agreement with a payment plan. However, be aware that penalties and interest will apply to that plan.

PEKIC/GETTY IMAGES

PEKIC/GETTY IMAGESYou can also settle your tax obligations using a debit card. While the fees are relatively low, you typically won’t earn significant travel rewards or cash back unless you opt for a product like the Amex Rewards Checking debit card, which gives you 1 point for every $2 spent on qualifying debit card transactions.

This spending rate, along with other factors, might suggest that using a different Amex Membership Rewards-earning card could be more advantageous.

The details regarding the Amex Rewards Checking debit card have been gathered independently by Dinogo. The information on this page has not been validated or endorsed by the card issuer.

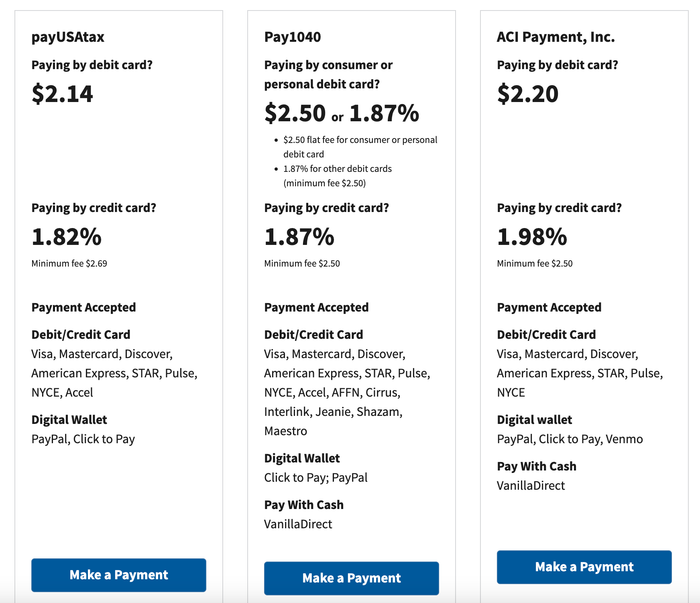

Fortunately, the IRS allows you to pay your tax bill via credit card through various third-party payment processors. However, be cautious: these companies often add their own fees to your payments. You can find a list of these companies and their convenience fees on the IRS website.

The expense of settling taxes with a credit card

When utilizing a credit card for tax payments, the fee is determined as a percentage of the total amount paid.

IRS.GOV

IRS.GOVCurrently, these fees range from 1.82% to 1.98%. Therefore, if you owe $10,000 and choose to pay by credit card, you’ll incur an additional $182 to $198 in fees, based on the service provider you select.

Advantages of paying your taxes with a credit card

Even with the added fees, there are numerous reasons why paying taxes with a credit card can be advantageous.

Firstly, this approach can help you accumulate valuable rewards and provide extra time to settle a large tax bill, especially if you have a 0% APR introductory offer on a new card or are eligible for a no-fee, pay-over-time plan. However, if your purchase is subject to standard credit card interest rates, it’s wise to explore other options, as spreading out payments could become very costly.

Here are some situations where using a credit card for your taxes could be beneficial.

Earning a substantial welcome bonus from your credit card

Many rewards cards offer welcome bonuses valued in the hundreds (and occasionally exceeding $1,000) in cash back or tens of thousands of points if you spend a specified amount on your new card within a designated timeframe.

The primary reason to use a credit card for a significant tax payment is the potential to earn a points bonanza from your initial spending on a new card. The value of the points earned can help mitigate the fees associated with using your card for taxes.

Some travel rewards cards come with particularly high minimum spending thresholds for earning bonuses, making a tax payment a perfect opportunity to meet that requirement.

Typically, using a card to pay taxes is beneficial only when you're aiming for a substantial welcome offer while also earning rewards at standard rates. If you can meet the minimum spending requirement without incurring the fees from tax payments, it’s advisable to simply mail a check to the IRS.

CLINT HENDERSON /Dinogo

CLINT HENDERSON /DinogoBefore opting to pay your taxes with a credit card, ensure you can settle your card balance in full. Failing to do so could result in interest charges and late fees that can easily overshadow any rewards you earn. Accumulating 20-25% interest on your credit card bill can quickly negate a 3-4% return from the points earned through spending.

Achieve a credit card spending requirement

Numerous credit cards provide rewards that activate once you meet a specific spending requirement. These thresholds may be based on the calendar year or your cardmember anniversary, but in either case, making substantial tax payments can help you qualify for these perks when that level of spending might otherwise be unachievable. For example:

- Spend $15,000 on eligible purchases with the Hilton Honors American Express Surpass® Card within a calendar year to receive a complimentary night certificate

- Earn an extra free night award valid at any Category 1-4 property after spending $15,000 on your World of Hyatt Credit Card each year following your cardmember anniversary

With benefits like these, charging your taxes to the appropriate credit card can enable you to earn valuable bonuses such as progress toward elite status, free night awards, and more.

Contribute toward elite status

Several credit cards allow you to enhance your elite status — or earn it outright — through your spending. Making a significant tax payment with one of these cards could be beneficial, including the following options:

- United℠ Business Card: Accumulate 25 Premier qualifying points (PQPs) for every $500 spent on the card, up to 1,000 PQPs per calendar year. This contributes to Premier 1K elite status

- American Airlines credit cards: Gain 1 Loyalty Point for each eligible dollar spent, helping to elevate your elite status through credit card use

- World of Hyatt Business Credit Card: Earn five tier-qualifying night credits for every $10,000 charged, aiding your quest for elite status with World of Hyatt

- World of Hyatt Credit Card: Receive two tier-qualifying night credits each year you maintain the card, plus earn two additional tier-qualifying night credits for every $5,000 spent

Utilize multiple cards to maximize your rewards

If you face a substantial tax bill, you aren’t required to pay the full amount with a single credit card.

The IRS page on credit card payments states that you can make up to two payments per tax period (year, quarter, or month, depending on the tax type) using debit or credit cards, allowing you to use two different cards for two separate payments.

For instance, suppose you have a tax payment of $28,000 due. You could apply for both The Business Platinum Card from American Express and the Ink Business Preferred® Credit Card. By charging $20,000 within three months of approval on the Amex Business Platinum Card, you'd qualify for the 150,000-point welcome bonus.

Additionally, since the purchase exceeds $5,000, you could earn 1.5 points per dollar (up to $2 million in these purchases per calendar year, then 1 point per dollar thereafter), resulting in 30,000 points from the purchase itself. Then, you could put the remaining $8,000 balance (within three months of approval) on the Ink Business Preferred, earning its welcome bonus plus an extra 8,000 points for that spending (1 point per dollar on everyday purchases).

In this scenario, you would accumulate over $6,000 in travel rewards, based on TPG's valuations. (These estimates do not consider the points earned from the fees charged for tax payments with these cards.)

Gain additional time to settle your tax bill

One of TPG's 10 commandments for maximizing credit card rewards is to avoid paying interest charges. It's crucial to ensure you never take on more than you can manage.

When using a credit card to pay your taxes, take note of when the first day of your new statement period starts on the card you intend to use. This allows you to have up to 30 days before your statement closes and nearly 60 days to fully pay off your balance.

Some credit cards offer 0% APR during an introductory period for new purchases, which can grant you 12-18 months of interest-free payments on your tax obligations. However, it's essential to pay off the entire balance before the promotional period ends to avoid steep interest charges.

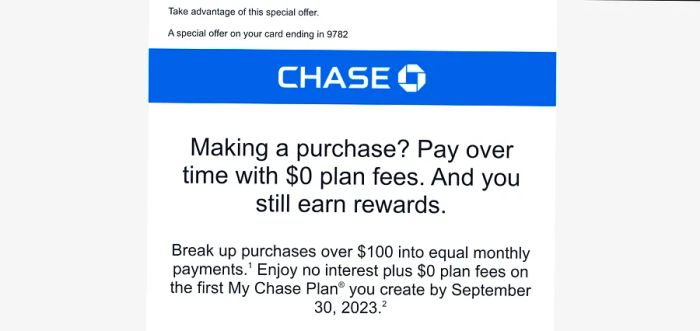

CHASE

CHASELastly, be sure to verify your eligibility for a pay-over-time installment plan, as some issuers may provide introductory offers.

For instance, TPG's senior editorial director Nick Ewen was targeted last year for a no-fee My Chase Plan on his Chase Sapphire Reserve®. For any purchase exceeding $100, he could have set up his first plan by Sept. 30, 2023, with no fees and no interest for the duration of the plan (typically between six and 18 months) — all while still earning rewards.

This can be an excellent method to manage a significant tax bill over time without facing hefty interest charges.

The drawbacks of paying your taxes with a credit card

Despite the aforementioned benefits, using a credit card for tax payments can be a risky move, as the interest rates on most rewards credit cards can significantly impact your finances if you're unable to pay it off.

If you lack a no-fee, 0% APR option and can't pay your statement balance in full after charging your taxes, it may be wise to rethink using a credit card for this purpose.

Instead, discuss your options with your tax professional. The IRS provides payment plans with interest rates that are generally lower than what most credit cards would offer.

In summary

Using a credit card to pay your taxes can be a rewarding way to accumulate points and miles as part of a generous welcome offer. If you have a 0% APR card, it may also allow you more time to settle a larger tax bill without the burden of high interest rates, but be sure to do the math to confirm that the advantages outweigh the costs.

The last thing you want is to find yourself repaying your taxes while dealing with exorbitant credit card interest rates.

1

2

3

4

5

Evaluation :

5/5