The approval of your next credit card depends on these three agencies

Your credit score significantly impacts your overall financial health. We often discuss what factors influence a credit score and how to maintain it effectively, but what are the sources of your score?

Let’s explore the three primary credit reporting agencies that calculate your score.

The three primary credit reporting agencies

The three leading credit reporting agencies—TransUnion, Equifax, and Experian—gather your financial data and create a report. These reports play a crucial role in determining your credit score, and they are accessed by banks and lenders when you seek a credit card, loan, or other credit options.

Stay informed about exclusive offers and check out our editors’ top credit card selections in our daily newsletter.

Each credit reporting agency utilizes its own approach to compiling your credit report and calculating your credit score, which is why your score might differ from one agency to another. Let’s delve into each agency and the scores they generate, and then we’ll explore which scores issuers consider when you apply for a new card.

TransUnion

Founded in 1968 as the parent company of Union Tank Car Company, a railcar leasing business, TransUnion entered the credit reporting sector in 1969 after acquiring the Credit Bureau of Cook County (CBCC). Since then, it has broadened its offerings beyond credit reporting but continues to be a leading credit bureau in the U.S.

A notable feature of TransUnion is its Identity Lock service. If you suspect that you have fallen victim to identity theft, TransUnion will freeze your report and notify Experian and Equifax about the freeze.

Equifax

Equifax is a leading global provider of data, analytics, and technology solutions. Similar to TransUnion, it serves as a significant credit reporting agency for lenders and also offers various financial services. The company gained considerable attention following a massive data breach in 2017 that impacted 147 million individuals. Since then, Equifax has undertaken a comprehensive security overhaul, recruited new leadership, and implemented measures to restore its reputation and enhance its security framework.

Experian

Completing the "Big Three" is Experian. In my experience, Experian excels in providing credit education resources. The company generates numerous annual reports based on its collected data and analytics. Naturally, Experian also delivers credit reporting and monitoring solutions.

Originally established as a forum in London in 1803, the company now known as Experian truly launched its credit reporting operations in the U.S. under the name TRW, which acquired Credit Data (another credit reporting agency) in 1968. The eventual merger of the London and U.S. entities led to the formation of Experian, the global powerhouse we recognize today.

CYTHER5/GETTY

CYTHER5/GETTYFICO vs. VantageScore

FICO and VantageScore represent the two main frameworks used by credit reporting agencies to assess credit scores. All three major agencies utilize these models to generate various types of scores. FICO is the older of the two, with a longer history, while VantageScore is the more recent model, created collaboratively by the three major credit reporting agencies in 2006.

Both scoring systems operate on a range from 300 to 850 — with a higher score indicating a more trustworthy borrower. Although there is considerable overlap in the criteria considered by each scoring model, there are also some nuanced differences between them.

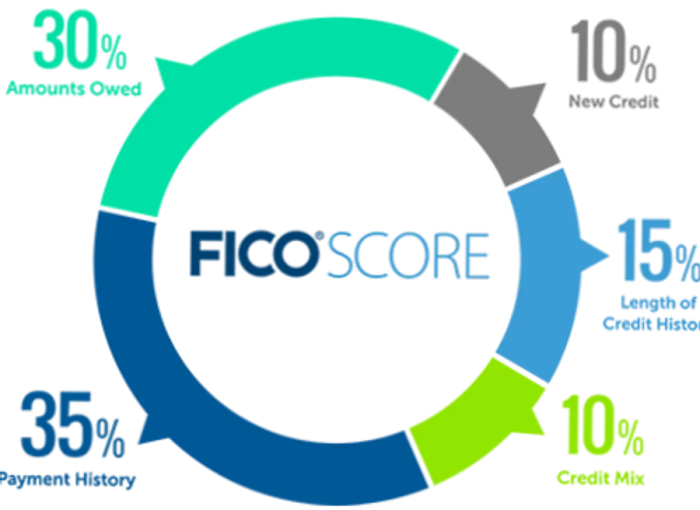

FICO

FICOFICO assigns specific percentage weights to each factor:

- Payment history (35%)

- Amounts owed (30%)

- Length of credit history (15%)

- New credit (10%)

- Credit mix (10%)

VantageScore maintains a more general approach in its formula, highlighting the relative importance of each factor:

- Payment history (extremely influential)

- Age and type of credit (highly influential)

- Percentage of credit limit used (highly influential)

- Total balances and debt (moderately influential)

- Recent credit behavior and inquiries (less influential)

- Available credit (less influential)

There isn't a universal credit score that every credit card issuer, bank, and lender uses. Additionally, each credit reporting agency may have different financial records on file. Consequently, your approval odds can vary based on which score is referenced for the decision-making process.

Which credit bureaus do banks consult?

When you apply for a credit card, the issuer reaches out to one (or more) credit bureaus to obtain a copy of your credit report. This report encompasses the categories previously mentioned. Understanding which credit reporting agency a card issuer relies on for reports can provide insight into your chances of approval.

You can leverage this knowledge to space out your applications (or combine them, if needed) in a manner that helps you sustain an optimal credit score, even if you are applying for several cards within a short period.

ISABELLE RAPHAEL/Dinogo

ISABELLE RAPHAEL/DinogoMany credit card issuers typically depend on a single bureau to handle credit card applications. However, the specific bureau they use to acquire reports may vary based on your state and the particular card you are applying for.

Here are some anecdotal data points reported over the years:

- Amex primarily utilizes Experian, though it occasionally pulls from Equifax or TransUnion.

- Capital One does not have a preferred bureau but often accesses more than one.

- Chase leans towards Experian, although it may also check Equifax or TransUnion reports.

- Citi typically retrieves credit reports from Equifax or Experian.

For instance, if you discover that Citi usually pulls from Equifax and Chase primarily relies on Experian, you could apply for cards from both issuers on the same day, potentially enhancing your approval odds for each.

Regrettably, credit card companies do not disclose which credit bureau they prefer. However, there are online platforms that compile customer feedback to provide an aggregate overview of which issuer uses which bureau.

These resources are not infallible and may reflect unverified (and possibly outdated) user contributions. Nevertheless, they can offer useful insights for your search, provided you recognize that the information may not be entirely accurate.

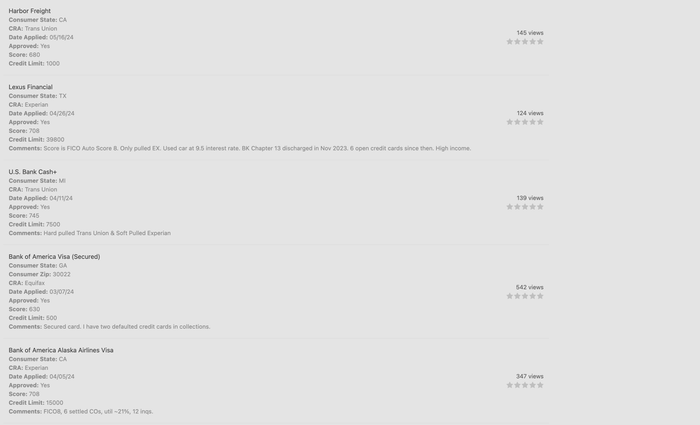

CreditBoards.com

The CreditPulls database on CreditBoards.com serves as a widely used online tool for insights into credit card applications. You can utilize this database to identify which credit report is likely to be accessed for your application and the score you might need to secure approval for a specific card. (Tip: Be sure to check the posting dates; the information may have changed since it was published.)

You can access the database by following these steps:

- Go to CreditBoards.com

- Select the CreditPulls option from the menu

- Choose your search criteria — including the applicant's state, credit reporting agency (CRA), application date, and approval status.

- Click "Update"

To explore a broader selection of card issuer options, simply enter your state and date range in the search criteria. For instance, I searched for data on credit pulls across the US for 2024. Here are some of the results:

CREDITBOARDS.COM

CREDITBOARDS.COMHowever, I want to emphasize that the credit bureau chosen by a card issuer to pull reports can vary not only by city but also by individual customer. To gain the clearest understanding, it's advisable to visit the site yourself and input your own details. Even then, your application outcomes may not match those of others.

This serves primarily as a guide to help you make an informed estimation about where an issuer might obtain your data.

Bottom line

When you apply for a new credit card, your issuer will retrieve information from one of the "big three" credit reporting agencies. Since the data provided by each agency differs (resulting in varying scores), it's crucial to keep track of your credit score with each company.

According to U.S. law, you are entitled to receive your complete credit report for free from each agency once a year. Make sure to take advantage of this opportunity to monitor your report and the information collected about you, even if you're also tracking your scores through your credit card issuer's mobile apps or other financial services.

1

2

3

4

5

Evaluation :

5/5