Why neglecting your credit cards might lead to losing them

Credit card companies prefer you to actively use your cards. A no-annual-fee credit card collecting dust in your drawer doesn't bring in any revenue for the issuer.

Moreover, having idle credit cards can pose risks. If you aren't monitoring your card, you might miss unauthorized charges made by thieves before you can alert the bank. This often leads banks to lower credit limits or shut down accounts for inactive cards.

Nonetheless, even if you seldom use certain cards, it's wise to prevent the issuer from closing your account or cutting your credit limit. Here's why keeping infrequently used accounts active can be beneficial and how to manage them wisely.

Stay informed on exclusive offers and see our editors’ top credit card recommendations by subscribing to our daily newsletter.

Reasons why banks shut down card accounts

Don't be taken aback if a credit card issuer decides to close a card you rarely use, whether it's in your wallet or hidden in a drawer. After all, issuers typically profit from customers in three main ways:

- Interest charges: If you carry a balance from month to month, you’ll incur interest. You can avoid this by paying your balance in full each month.

- Consumer fees: Costs like annual fees, late fees, cash advance fees, and balance transfer fees can often be avoided but may offer valuable benefits and conveniences.

- Merchant processing fees: When you swipe your credit card, the merchant incurs a processing fee.

MSTUDIOIMAGES/GETTY IMAGES

MSTUDIOIMAGES/GETTY IMAGESIssuers seek cardholders who generate profits through these fees. Therefore, they prefer to extend credit to customers who actively use their cards and reliably make payments.

However, issuers must also mitigate the risk associated with unprofitable cardholders, particularly those with high credit limits but low usage. As a result, they may opt to reduce the credit limit on rarely used accounts or even close accounts that are not in use.

Reasons to keep your card accounts active

When one of your credit accounts is closed, it typically leads to a drop in your credit score. For instance, when my mother-in-law closed her cobranded Southwest credit card last year, her credit score fell by about 20 points.

There are five key factors that determine your credit score, and closing an account can adversely affect two of them: credit utilization and the duration of your credit history.

CNYTHZL/GETTY IMAGES

CNYTHZL/GETTY IMAGESCredit utilization

When an account is closed, your available credit decreases. This reduction negatively impacts your credit utilization ratio. For instance, if you have $3,000 in credit card debt spread across four cards, each with a $5,000 limit, you are using $3,000 of your $20,000 total limit — that’s 15%. If one card is closed, you’ll then be using $3,000 of a $15,000 total limit, raising your utilization to 20%. Thus, your ratio spikes even though your debt remains unchanged.

Ideally, you should maintain your credit utilization ratio below 20-30%. If an issuer closes your account or lowers your credit limit, you’ll need to reduce your credit card debt or boost your available credit to maintain the same ratio. You can achieve this by paying down your debt or requesting a credit limit increase from another issuer. This helps mitigate the impact on your credit score when a card is closed.

Length of credit history

Your credit score may also suffer if the closed credit card is one of your oldest accounts. The length of your credit history is a significant factor in determining your credit score. If the average length of your credit history decreases due to a closed account, your credit score could drop. Therefore, it’s crucial to make an effort to keep your oldest accounts active.

Tips for keeping rarely used card accounts active

There are several reasons you might not frequently use a particular card. However, it's important to keep all your cards in good standing, especially if they could be beneficial in the future or are among your oldest accounts. Here are two strategies to consider.

JACOB LUND/SHUTTERSTOCK

JACOB LUND/SHUTTERSTOCKMake at least one purchase on each card every six months

Typically, you should use each account at least once every six months to maintain its active status. My husband and I check all our accounts biannually and transfer $5 from each seldom-used account to my Amazon Gift Card balance. This approach ensures the accounts remain active. We then use our Amazon balance to buy gift cards and other necessities.

There are various ways to ensure regular spending on your cards. For instance, consider setting up at least one subscription service—like Hulu or Spotify—on each card. You might also assign specific cards for different categories of expenses, such as gas, groceries, restaurants, travel expenses, and charitable contributions. If you choose this method, make sure to pair each card with the categories where they offer the best rewards.

Nonetheless, based on a notice received by two TPG employees, you might want to use your cards more often than just once a year.

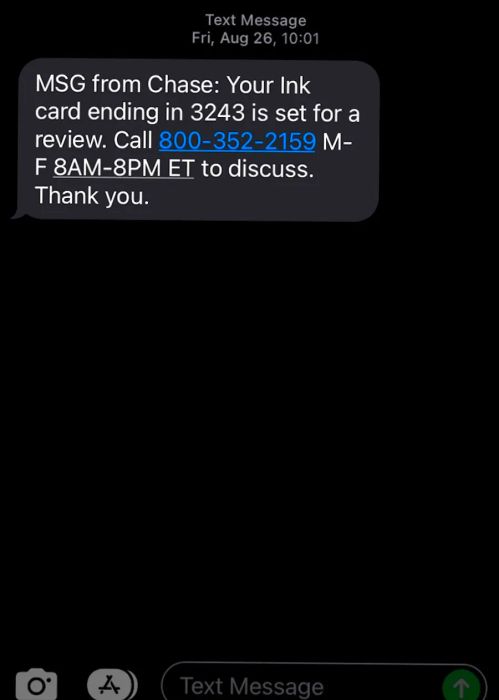

RYAN SMITH/Dinogo

RYAN SMITH/DinogoIn August 2022, TPG contributor Ryan Smith got a text from Chase informing him that one of his Ink business cards was under review and might be closed due to inactivity. Despite setting a reminder to use his older credit cards every 90 days, Ryan hadn’t touched this particular card at all in 2022, leaving it inactive for nearly nine months before receiving this alert.

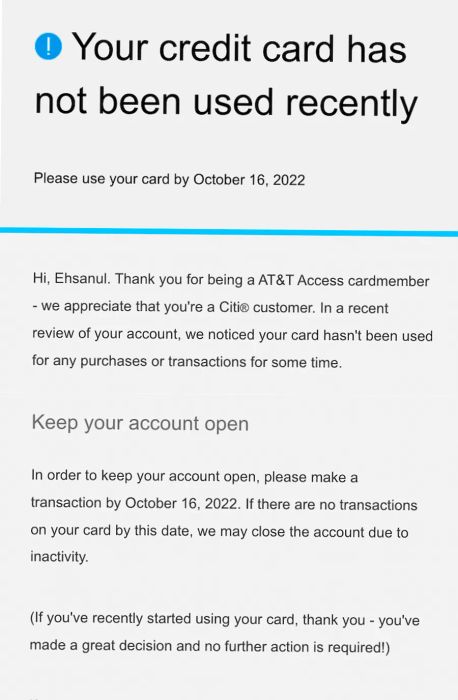

Points and miles contributor Ehsan Haque received a similar warning, giving him just over a month to use his inactive credit card before the bank would close it. Before this notification, Ehsan had not used this specific credit card for more than eight months.

EHSAN HAQUE/Dinogo

EHSAN HAQUE/DinogoBe alert for closure alerts

Some credit card issuers will give cardholders a heads-up about a potential account closure, while others may proceed without any prior notice. If you receive a notification indicating that your card account will be — or has already been — closed, you might be able to keep it open by contacting your issuer and explaining your situation.

For instance, a few years back, I got a notice stating that my cobranded United Airlines credit card was set to be closed. I called the number on the back of my card and shared my reasons for wanting to retain it. Although I hadn’t used the card in the previous year, I mentioned that I planned to travel with United more often in the future, which would lead to increased usage. The agent agreed to keep my account open, but this situation could have been avoided if I had used my card a few times each year.

Ensure your contact details are current with your credit card issuers. This way, you'll receive emails, texts, or letters alerting you to any upcoming account closures.

Key takeaways

As inflation persists, it's crucial to protect your credit score against potential recession impacts. One effective strategy is to regularly use your seldom-used cards, as card issuers are less likely to close accounts that show activity. Ideally, aim to make a purchase on each card at least once every six months to keep them active.

Keeping your card accounts open is important for maintaining your account history and credit utilization, particularly for cards with high limits or a long history — both of which can enhance your credit score.

Evaluation :

5/5