Credit Cards 101: A Guide for Beginners

At TPG, we have a passion for credit cards. We've seen firsthand the benefits of earning rewards and want to share that experience with everyone.

If you're just starting with credit cards, you might find reading an application (or even a review) feels like a class you weren't enrolled in. If that sounds familiar, you're in the right place.

We're here to demystify credit cards for you. We’ll discuss everything from terminology to different card types and even how to interpret your credit card statement. So, get comfortable, grab a notepad if you like, and let’s dive in.

Sign up for our daily newsletter to receive updates on exclusive offers and to compare our editors’ favorite credit card selections.

Understanding Credit Card Debt

Before diving deeper, it’s crucial to highlight that while we at TPG appreciate credit cards, we strongly advise against carrying a balance. Doing so incurs interest charges, which can far exceed the value of any rewards you might earn.

JLCO-JULIA AMARAL/GETTY IMAGES

JLCO-JULIA AMARAL/GETTY IMAGESIf you’re thinking about applying for a credit card, ensure you have a solid plan to adhere to your budget and pay off your balance every month. Only use your credit card for purchases if you are absolutely certain you can cover them when the bill arrives.

Understanding Credit Scores

A credit score is a numerical value—ranging from 300 to 850—that lenders assess to gauge their risk in loaning you money.

VIKTORIIA ABLOHINA/GETTY IMAGES

VIKTORIIA ABLOHINA/GETTY IMAGESYour credit score consists of several elements, such as payment history, total debt, and any new credit accounts. To establish and maintain a strong credit score, it’s essential to borrow responsibly and repay on time. Regularly using your credit card and paying off the balance in full each month is an excellent strategy to boost your credit score.

When you seek any form of credit, including a credit card, lenders will review your credit score to assist in their decision-making process regarding your application. Generally, top rewards cards require good to excellent credit scores for approval.

If your score isn't where you'd like it to be, don't be concerned. We can guide you on how to enhance your credit score and even earn rewards while you improve your credit.

Debit vs. credit cards

Using a debit card means that funds are directly withdrawn from your bank account to pay for your purchase. This is why a $1,000 transaction will be declined if you only have $500 in your account.

In contrast, a credit card allows you to borrow money from the credit card issuer to complete your purchase. When you settle your balance, you are essentially repaying them for the amount borrowed. If you do not pay within the specified period (usually about a month), you will incur fees and interest, which can negatively impact your credit score.

WESTEND61/GETTY IMAGES

WESTEND61/GETTY IMAGESThe primary advantage of using a debit card is that it helps you avoid overspending. However, if you use a credit card wisely, you can earn rewards, access extra perks, and enhance your credit score.

Understanding your credit card statement

Navigating the various terms, dates, and figures on a credit card statement can feel like solving a puzzle. Fortunately, it’s simpler than it seems once you grasp some essential terms.

Let’s differentiate between the terms "bill" and "statement." Traditionally, cardholders would receive a physical statement (or bill — the two terms are often interchangeable) in the mail every month. This document would summarize the cardholder's expenditures for the billing cycle (the period since the last bill), the statement balance (the total amount charged during that cycle), the minimum payment due, and the payment deadline.

10'000 HOURS/GETTY IMAGES

10'000 HOURS/GETTY IMAGESToday, we enjoy the convenience of online account access at any moment. While we still receive statements that detail our billing cycles, we can also track transactions made since the previous statement. This added information is beneficial but can also lead to some confusion.

Here’s what you might encounter when you access your online account:

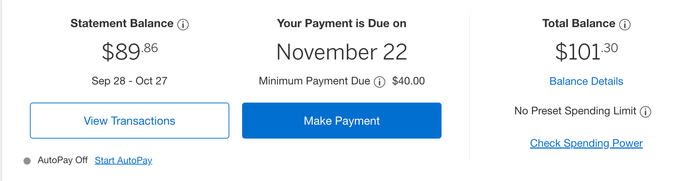

AMERICAN EXPRESS

AMERICAN EXPRESSThe statement balance represents the total charges incurred during your latest billing cycle. To prevent incurring interest or late fees, this amount must be settled by the due date.

The due date for your billing period varies by card, and you can locate this information in your card’s terms and conditions.

For instance, in the scenario above, the cardholder is required to pay their statement balance of $89.86 by the due date of Nov. 22 to avoid any fees.

The minimum payment is the smallest amount you can pay by the due date to avoid incurring a late fee. However, if you only pay the minimum (or less than the total statement balance), you'll carry a balance into the next billing period and be charged interest on that amount.

The "total balance" indicates the full amount owed on your card: the previous month's statement balance plus any charges made since the last billing cycle ended. In this case, the cardholder has added $11.44 since the closing date, making the total balance $89.85 plus $11.44. They can either pay the total balance or just the statement balance to avoid fees. If they choose the latter, the $11.44 will appear on the next bill for the following month.

Another figure you’ll likely see is "available credit," which shows how much of your credit limit remains. This amount changes as you pay off your balance or incur additional charges. For instance, if the user’s credit limit is $4,000, their available credit would be $3,898.70 (the total balance of $101.30 subtracted from the credit limit). It’s best to avoid reaching your credit limit, as exceeding it could result in denial of charges or over-the-limit fees.

Rates and fees

Now that you know how to manage your credit card bill, let’s go over the key fees a credit card issuer may apply.

- Annual percentage rate (APR): This is the yearly interest rate applied to your balance. Different types of APRs exist, such as those for balance transfers, cash advances, penalties, and purchases. The most prevalent is the purchase APR, which is the monthly interest rate applied if the statement balance isn’t paid off in full.

- Introductory APR offer: A temporary lower APR can help you save on interest charges for purchases and balance transfers.

- Annual fee: This is the annual cost for maintaining your card, typically charged once a year. Some cards don’t have an annual fee, while others may charge up to $550 or more annually.

GEBER86/GETTY IMAGES

GEBER86/GETTY IMAGES- Foreign transaction fee: This fee is incurred when you make a payment in a foreign currency. Some credit cards do not charge foreign transaction fees, while others can impose fees of up to 3% for each transaction.

- Late payment fee: This is charged when you fail to meet the minimum payment by the due date. In addition to this fee, you may incur a penalty APR on your balance.

- Over-the-credit limit fee: This fee is applied when you exceed the credit limit set on your card.

- Return payment fee: Charged when your payment method fails or bounces, which may occur due to insufficient funds or account issues.

Types of credit cards

If you’re new to credit cards, the variety of options can be daunting. It’s beneficial to start by deciding which type of credit card suits your needs best.

Here are the most popular types of credit cards.

General travel

These credit cards offer travel rewards and come with various perks not linked to specific airlines or hotel chains. They usually provide transferable rewards, which are highly valued for their versatility and worth.

CATHERINE FALLS COMMERCIAL/GETTY IMAGES

CATHERINE FALLS COMMERCIAL/GETTY IMAGESAdditionally, these cards often include general travel benefits like travel insurance, TSA PreCheck/Global Entry credits, and access to airport lounges.

For our top recommendations, check out our complete list of the best travel credit cards.

Airline

Airline credit cards are linked to a specific airline. You’ll earn rewards in that airline’s points or miles and enjoy benefits such as complimentary checked bags, automatic elite status, and access to airport lounges.

For our top choices, explore our complete list of the best airline credit cards.

Hotel

Hotel credit cards are associated with a specific hotel chain. You’ll earn points that can be redeemed at any hotel within that brand, along with perks like complimentary nights and automatic elite status.

HILTON

HILTONFor excellent hotel cards, check out our complete list of the best hotel credit cards.

Cash-back

Cash-back cards are typically the easiest to earn and redeem rewards. With a cash-back card, you earn a percentage of your purchases back in rewards, which can then be redeemed for cash—either as a statement credit, a mailed check, or direct deposit into a qualifying checking or savings account, depending on the card issuer.

To explore some of our top cash-back card options, check out our complete list of the best cash-back credit cards.

Secured

A secured credit card is an excellent choice for those with limited credit history or lower credit scores. When you open a secured card, you’ll make a security deposit that serves as collateral for the credit card issuer.

IPPEI NAOI/GETTY IMAGES

IPPEI NAOI/GETTY IMAGESTypically, these cards do not offer rewards, but they are a valuable tool for building your credit and enhancing your chances of qualifying for a rewards credit card in the future.

For some excellent choices, check out our complete list of the best secured credit cards.

Student

A student credit card is specifically designed for college students. These cards aim to help students establish credit, cultivate sound financial habits, and foster a relationship with a bank, preparing them for more sophisticated credit cards after graduation.

While they usually offer limited rewards, they provide a solid introduction to the world of credit cards for students.

For some student-oriented options, check out our complete list of the best credit cards for college students.

Authorized user

An authorized user is an individual who has been added to someone else's credit card account by the primary cardholder. This user can make purchases using the card but typically enjoys limited benefits.

BLACKCAT/GETTY IMAGES

BLACKCAT/GETTY IMAGESIf you’re struggling to get approved for a credit card, becoming an authorized user on another person's account can positively impact your credit score.

Earning rewards

Each rewards card accumulates a specific type of rewards "currency." For instance, the American Express® Gold Card earns transferable American Express Membership Rewards points, the Citi® / AAdvantage® Platinum Select® World Elite Mastercard® earns American Airlines AAdvantage miles, and the Hilton Honors American Express Surpass® Card earns Hilton Honors points. These currencies have varying values, so refer to our TPG valuations chart for insights on each rewards type's worth.

The amount of rewards you earn depends on your card’s earning rate and your spending habits. Some cards offer a fixed rate, providing the same reward amount for every purchase. For example, the Capital One Venture Rewards Credit Card earns 2 Capital One miles for every dollar spent, while the Citi Double Cash® Card offers 2% cash back on all purchases (1% at the time of purchase and another 1% when you pay).

MLADENBALINOVAC/GETTY IMAGES

MLADENBALINOVAC/GETTY IMAGESOther cards feature bonus-earning categories. For instance, the Chase Sapphire Preferred® Card earns 3 Ultimate Rewards points for every dollar spent on dining, popular streaming services, and grocery delivery, along with 2 points per dollar on travel purchases. It earns 1 point per dollar on all other transactions.

Additionally, many rewards cards offer a welcome bonus that can be highly valuable (potentially worth hundreds or thousands of dollars). To qualify for the welcome bonus, you must spend a specific amount of money within a designated timeframe.

The information regarding the Citi® / AAdvantage® Platinum Select® World Elite Mastercard® has been independently gathered by Dinogo. The card details presented on this page have not been reviewed or supplied by the card issuer.

Credit card best practices

You may have heard that credit cards can lead to serious financial trouble. While we don’t advise avoiding credit cards altogether, we advocate for their responsible use.

Here are some of the best credit card practices that we follow.

Always pay your balance on time and in full. We cannot stress this enough. If you start accumulating interest charges, you’ll negate any points and miles earned, and carrying a balance can quickly lead to substantial debt.

Credit cards are not free money, so never spend more than you can afford. Remember that you'll need to pay the statement balance on your card every month. Budget carefully and manage your credit wisely to keep your finances in check.

MSTUDIOIMAGES/GETTY IMAGES

MSTUDIOIMAGES/GETTY IMAGESBe aware of credit card application restrictions. While it may be tempting to jump straight into maximizing credit card rewards, it’s wise to take a measured approach. Not only should you give yourself time to establish a credit card budgeting system that suits you, but also remember that some issuers have their own restrictions. It’s beneficial to have a thoughtful, long-term strategy before applying for a credit card.

Wait at least three months (preferably six months or more) between applications. Opening new credit lines can affect your credit score, and applying for too many cards too quickly raises red flags. Take your time to earn a card's welcome bonus and assess how well the card fits your lifestyle before selecting your next card to enhance your wallet.

Consider carefully before canceling a credit card. As you accumulate more cards, you might be tempted to cancel those you don’t use frequently. However, if a card has no annual fee, there’s little downside to keeping it. The length of your credit history impacts your credit score, so maintaining your oldest cards can help improve your credit profile.

Crafting a points-and-miles strategy

Now that you've grasped the basics of credit cards, it's time to select the right one for you.

You don’t have to establish a strategy immediately. If the variety of rewards feels daunting, consider starting with a cash-back card to reinforce good credit habits while enjoying straightforward rewards redemption.

FRAZO STUDIO LATINO/GETTY IMAGES

FRAZO STUDIO LATINO/GETTY IMAGESHowever, if you have a specific dream trip in mind, you might want to focus on a travel rewards card that can help turn that dream into a reality.

When you're ready to dive into a points-and-miles strategy, take a look at our TPG guide to getting started with points and miles for travel.

In conclusion

Well done! You now have the essential terms and insights needed to research, apply for, and use a credit card responsibly.

Next, explore our suggestions for the best first credit cards and leverage your newfound knowledge to select the one that aligns with your spending habits and rewards objectives. We're here to support you on every step of your credit card journey.

1

2

3

4

5

Evaluation :

5/5